The global SEO services industry crossed $100 billion for the first time in 2026. It is also the most disrupted year the agency business has had in a decade.

Underneath the headline growth — 12% to 17% CAGR depending on whose forecast you read — annual client churn sits at roughly 38% for SEO agencies, AI Overviews now appear on 15–30% of Google queries depending on the dataset, and 61% of agencies are scrambling to add AI-search optimization to their service menus. SEO job listings dropped 37% year-over-year in early 2024, while top enterprise agencies report record growth. Both stories are true at once.

This post pulls together the data from a dozen primary sources — Conductor, Backlinko, Ahrefs, Semrush, SE Ranking, Pew Research, Mordor Intelligence, IBISWorld, the Business Research Company, Focus Digital, First Page Sage, seoClarity, Editorial.link, and HubSpot — into a single neutral snapshot. No advocacy, no take. Just the numbers.

The headline numbers

Metric

2026 value

Source

Global SEO services market

$83.98B – $108.28B

Mordor / TBRC

Grow your organic traffic from chat-bots

Track your AI visibility across ChatGPT, Gemini, Claude, and Perplexity — and turn chat-bot mentions into traffic.

Setup in 60 seconds

Cancel anytime

Keep reading

Related posts

More articles on the same topics, prioritized by shared tags and keyword overlap.

Projected market size by 2030

$203.83B

Research and Markets

US SEO/marketing consulting firms

~363,000

IBISWorld

Average agency monthly retainer

$3,209

Ahrefs (439 providers)

Average SMB monthly SEO spend

$497

Backlinko (1,200 owners)

Annual SEO agency churn

~38%

Focus Digital

Agencies adding AI Overview optimization

61%

SE Ranking

AI Overviews appearing on Google queries

15–30%

Semrush / seoClarity

1. Market size & growth

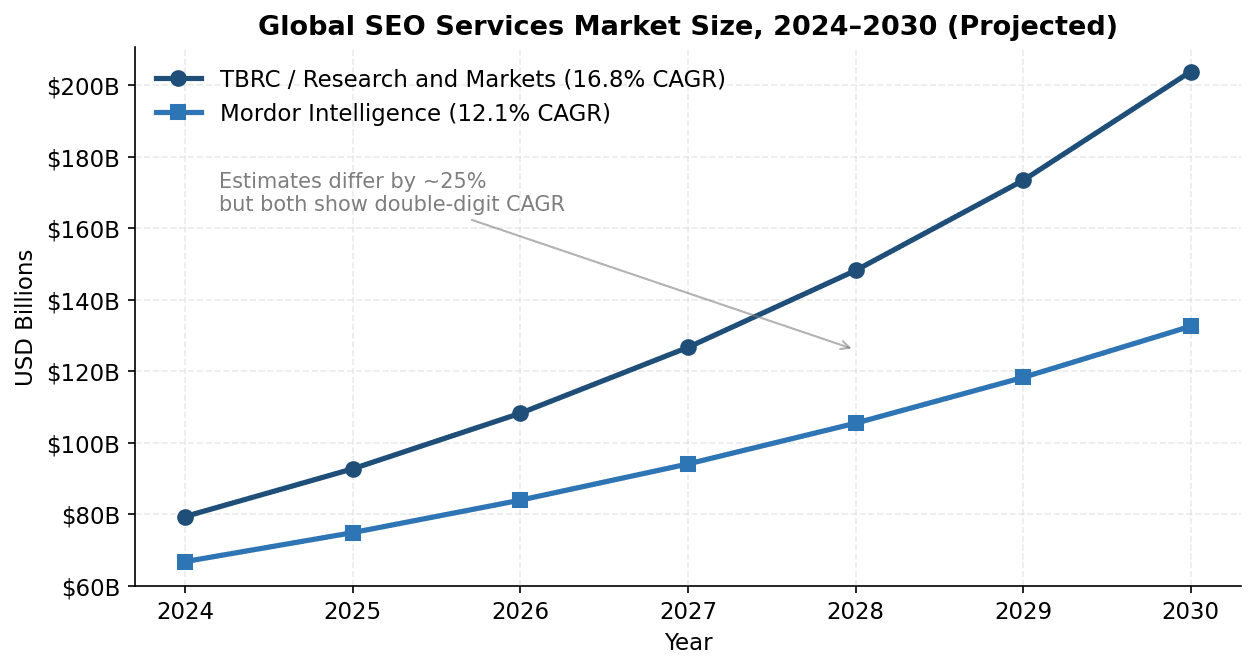

The 2026 estimate for the global SEO services market sits between $83.98 billion (Mordor Intelligence) and $108.28 billion (The Business Research Company). The discrepancy comes down to scope: narrower definitions exclude internal SEO tooling and some consulting revenue. Both sources project double-digit CAGR through 2030.

Research and Markets puts the global agency-only segment at $87.82B in 2026, growing to $165.29B by 2030. IBISWorld counts roughly 363,000 active SEO and internet marketing consulting firms in the US, growing at a 21.9% five-year CAGR in firm count. The US alone reportedly accounts for $119.4B in consulting revenue (a broader definition than agency-only).

Two leading market-research firms agree on the trajectory; they disagree on the absolute size by ~25%.

Regional breakdown

Region

2025 revenue share

CAGR through 2031

North America

33.9%

~12%

Europe

~28%

~11%

Asia-Pacific

~25%

13.55%

Rest of world

~13%

~10%

North America still dominates, but Asia-Pacific is the fastest-growing region. APAC growth is concentrated in India, Indonesia, and Vietnam, where SMB digitalization and English-language SEO talent are scaling in parallel.

2. What agencies charge in 2026

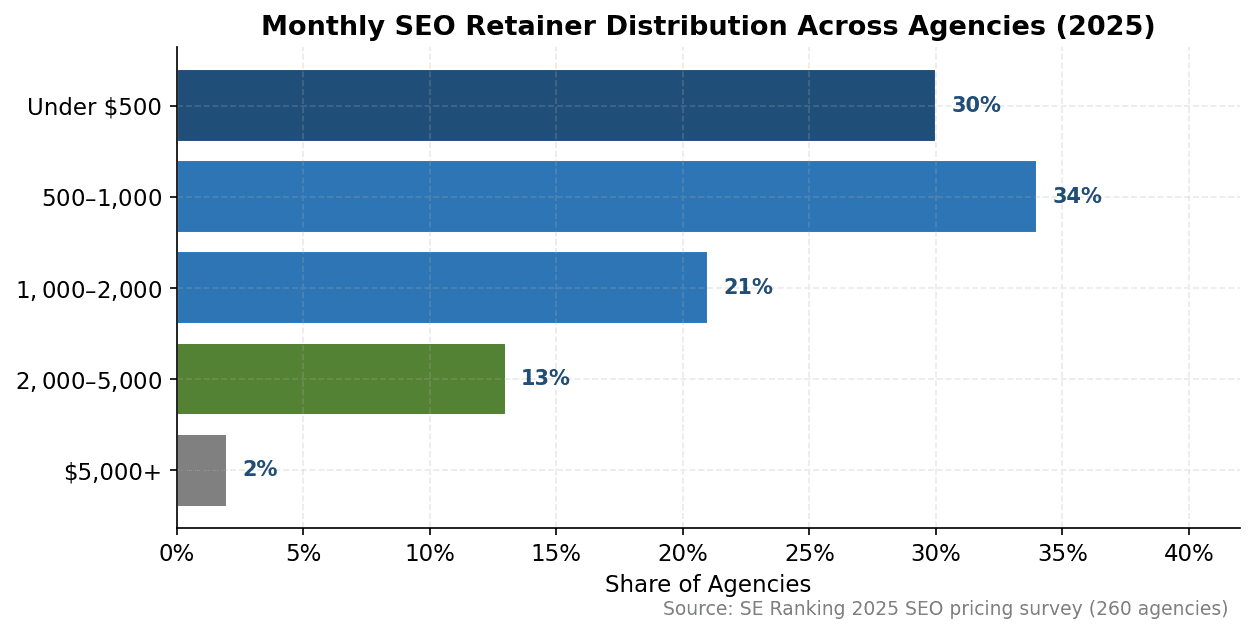

Two large 2025 surveys frame 2026 pricing. SE Ranking surveyed 260 agencies; Ahrefs polled 439 SEO providers. Their combined picture is unambiguous: most SEO is sold for less than $1,000 a month, and the gap between freelancers and agencies is roughly 2.4x.

64% of agencies still price retainers below $1,000/month; only 15% charge above $2,000.

Notable detail: 70% of agencies raised prices in 2024–25, citing inflation, operational costs, and AI tooling investment. But at the SMB end, the average US small business spends just $497.16/month on SEO (Backlinko's 1,200-owner panel), and clients spending under $500 are 75% more likely to be dissatisfied than those spending more — a structural mismatch between SMB budgets and what agencies say is needed.

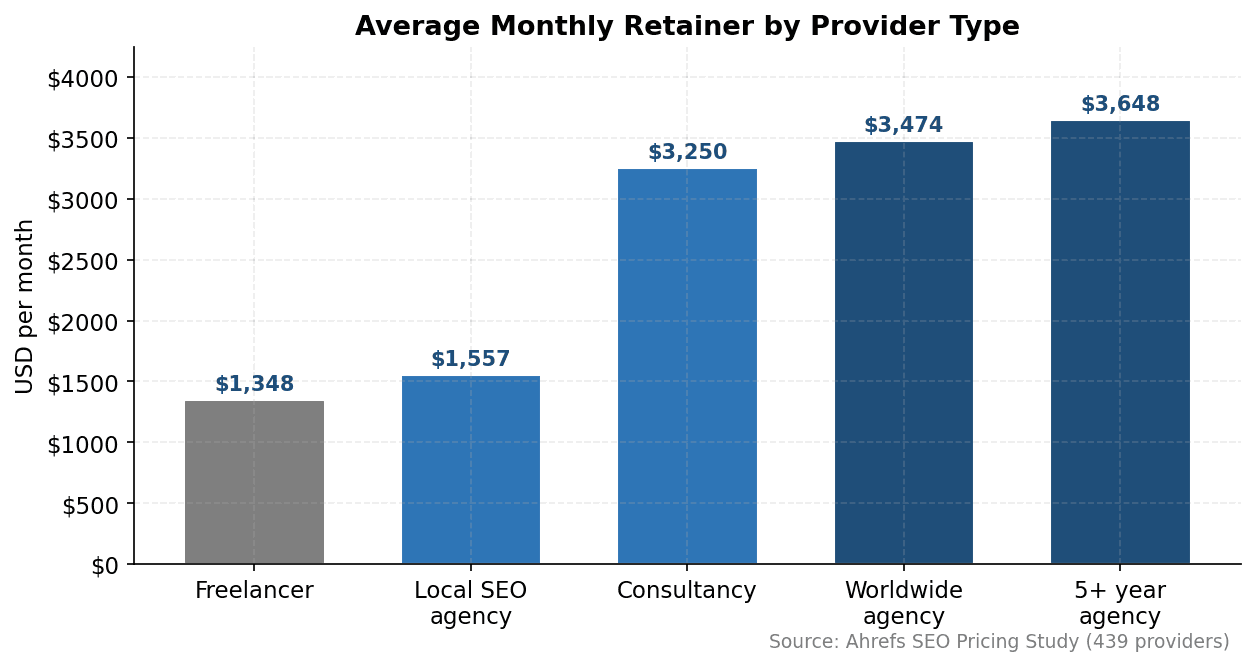

Agency tenure matters: shops in business 5+ years charge more than double those under 2 years.

Hourly rates and project pricing

Average hourly rate: $111 across all providers (Ahrefs).

Most common bracket: $75–$100/hour (24% of respondents).

Project-based pricing: 48.9% of providers offer it; average project ranges from $2,500 (audits) to $25,000+ (technical migrations).

Local SEO retainers: $1,557/month average; worldwide-serving providers charge 123% more ($3,474/month).

Enterprise programs: $5,000–$50,000+/month; 81% of B2B companies expect to spend at least $7,500/month on SEO (Conductor).

The SMB pricing mismatch

SE Ranking found 64% of agencies charge below $1,000/month and 30% under $500.

Backlinko's panel found the average US SMB spends $497.16/month — putting most SMBs in the bottom-third pricing tier.

75% of SMBs spending under $500/month report dissatisfaction with their provider.

The data suggests SEO is being sold at a price point most providers admit they can't deliver outcomes at.

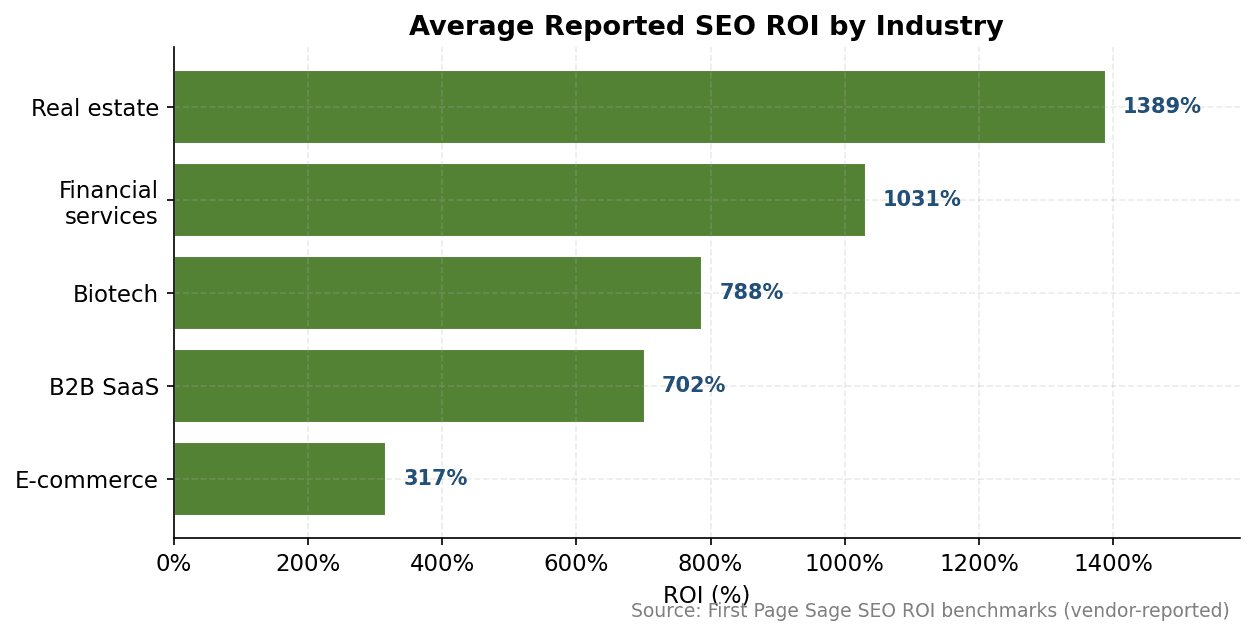

3. Performance, ROI & time-to-results

First Page Sage's industry benchmarks remain the most-cited ROI dataset. Average breakeven on SEO investment is 6 to 12 months, with peak ROI hitting in years 2–3. SEO leads close at 14.6% versus 1.7% for outbound (Doyen Digital / Intergrowth), and SEO is widely reported to reduce customer acquisition cost by approximately 61% versus paid acquisition.

Note: ROI figures are vendor-published industry medians. Treat as directional benchmarks, not audited returns.

Time-to-results expectations vs. reality

Industry-cited average: 6–12 months to breakeven (First Page Sage, Backlinko).

Backlinko panel reality: The average client gives a provider about 2 years before switching.

Practitioner consensus: 71% of SEO professionals say AI-era results take longer to materialize than pre-2023 baselines.

First-page rankings: Backlinko data: only 5.7% of newly-published pages reach Google's top 10 within a year.

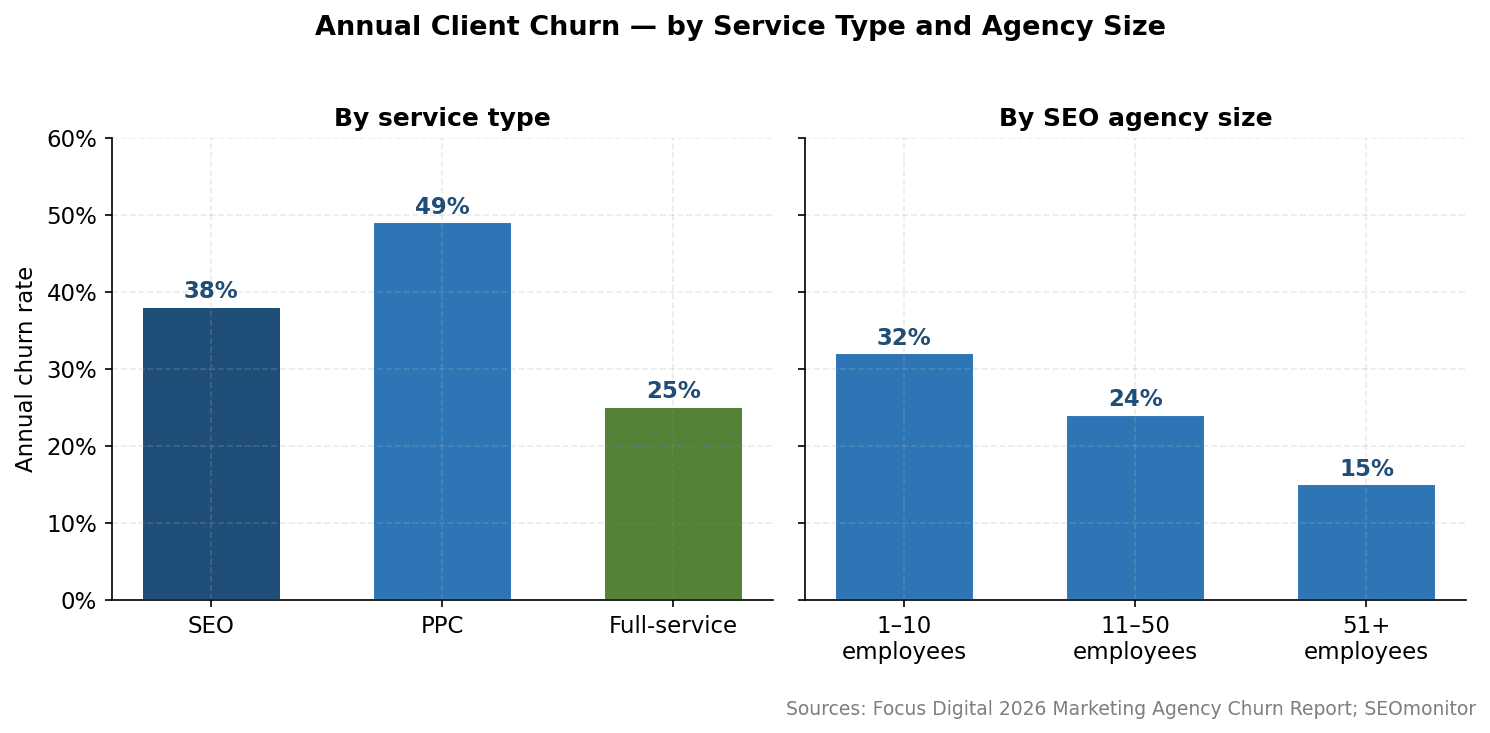

4. Client retention & churn

Industry research from Focus Digital's 2026 Marketing Agency Churn Report, SEOmonitor, and Sakas & Co. converges on a clear picture: SEO has lower annual churn than PPC but higher than full-service agencies.

Larger SEO agencies retain clients dramatically better than small shops — likely a function of senior staffing, processes, and the ability to offer multiple service lines.

Retention benchmarks

Contract type

Annual churn

Average lifespan

Retainer-based

18%

~56 months

Project-based

42%

~24 months

SEO industry average

38%

~32 months

Healthy benchmark

≤20%

60+ months

Backlinko's panel adds nuance: 65% of SMBs have used 2 or more SEO providers, and 10% are 'rapid switchers' who cycle through 3+ providers a year. The implication is that the lower-tier of the SMB market is structurally unstable for agencies — clients arrive cheap, leave fast, and don't refer.

Why clients fire agencies

Synthesized across Search Engine Land's "Six Reasons to Fire Your SEO Agency," Focus Digital's 2026 churn report, OnTheMap, Marketer's Center, and Rock The Rankings:

Misaligned expectations set during the sales process ("results in 90 days" promises that don't materialize).

Stagnant or declining traffic after 12+ months of work.

Reporting that doesn't tie to revenue — vanity metrics, no business-impact narrative.

Account manager turnover and "junior-on-the-account" delivery at scaled agencies.

Slow adaptation to AI search — increasingly cited in 2025–26 ("our agency hasn't mentioned AI Overviews in any monthly report").

Lack of transparency around tactics, especially link building.

Communication gaps — multi-day email response times.

5. Services & deliverables in 2026

SE Ranking's agency survey found 85% of agencies bundle services into packages, and 93% cross-sell PPC, social, web design, or maintenance. The pure-play SEO agency is increasingly rare — most agencies are positioning as growth or organic-marketing partners with SEO as the lead service.

What's in a standard 2026 mid-tier retainer

Deliverable

Standard inclusion

Notes

Technical SEO / Core Web Vitals

Yes

Universal across all retainers

On-page optimization

Yes

41.8% of agency revenue (Mordor)

Content production (4–8 pieces/mo)

Yes

Increasingly AI-assisted

Keyword research

Yes

Universal

Link building

Yes

32% of typical SEO budget

Monthly reporting

Yes

Shifting to revenue-based

AI visibility tracking

New in 2026

61% of agencies adopting

Schema / entity work

Increasingly

GEO-driven inclusion

Mordor Intelligence's segmentation: on-page SEO held 41.8–42.3% of agency revenue share in 2025; voice and visual search SEO is the fastest-growing sub-segment at ~20% CAGR. Retainer/subscription contracts represented 61.95% of 2025 revenue, but outcome-based contracts are growing fastest at 18.4% CAGR — a clear signal that clients are pushing for accountability.

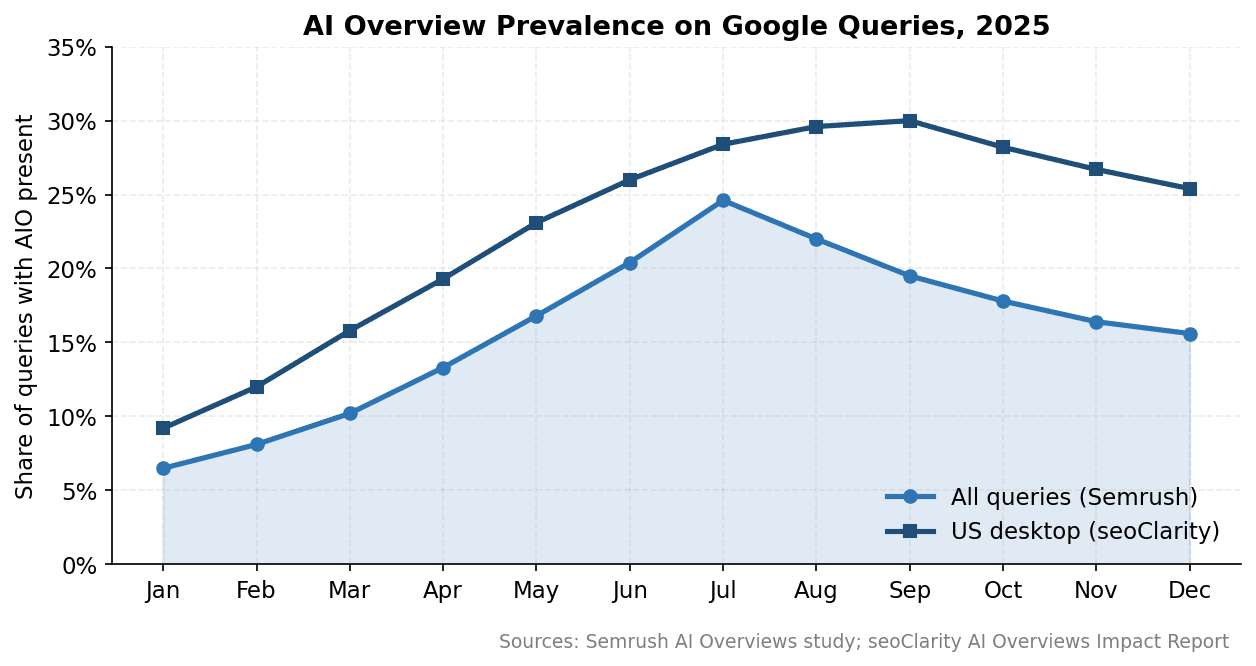

6. The AI / GEO disruption

This is the section where the data has changed the most year-over-year. Three things are happening simultaneously: AI Overviews are appearing on more Google queries, click-through rates are dropping when they appear, and agencies are repackaging their services to include AI search visibility.

AIO prevalence climbed sharply through mid-2025, then settled. Desktop and mobile diverge — desktop sees AIOs more often.

AI Overviews appeared on just 6.49% of US queries in January 2025 (Semrush). By July, that had risen to 24.61%. seoClarity's desktop-only dataset put AIO prevalence at 30% of US desktop queries by September 2025 — roughly a 492% year-over-year increase.

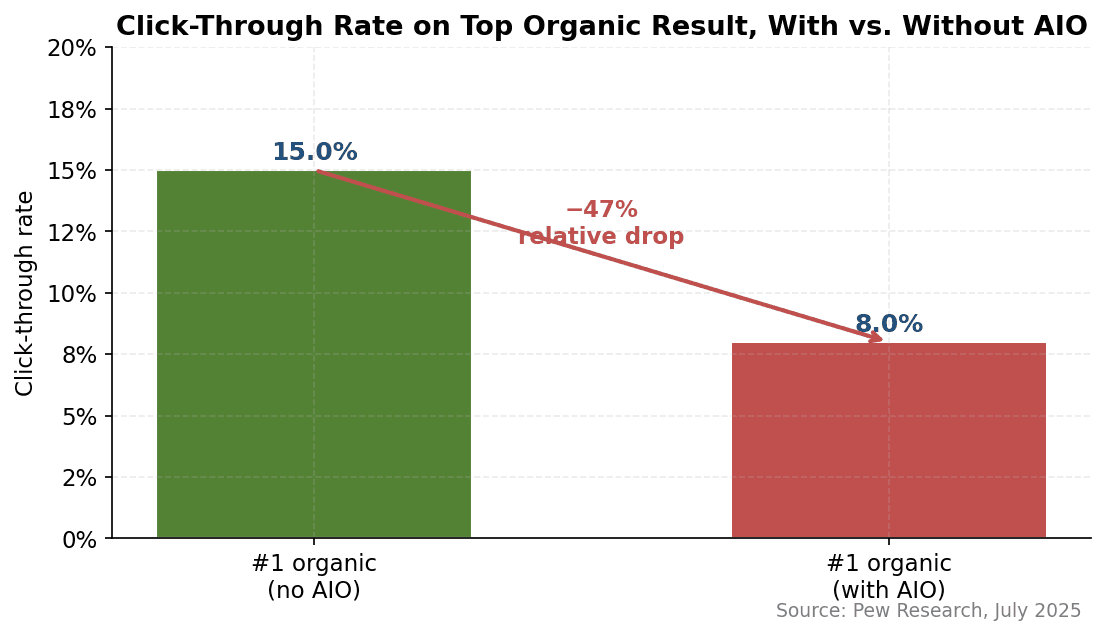

Pew Research, July 2025: when an AI Overview appears, the top organic result loses nearly half its clicks.

The traffic implications are now clear in the data. Multiple studies report a 34.5% CTR decline on the #1 organic result when an AIO is present. Pew Research found CTR drops from 15% to 8% — a 47% relative decline. Roughly 60% of all Google searches now end without a click (Bain, February 2025), and 27.2% of US searches end without a click specifically because of AIOs (Search Engine Land).

How agencies are responding

SE Ranking's 2025 survey produced the most quotable agency-side statistic of the year: 61% of agencies are considering adding optimization for AI Overviews and other AI engines. 43% plan to integrate AIO optimization into existing offerings; 18% plan to sell it as a standalone service. The average set or planned monthly fee for AIO-only services is approximately $937/month — a deliberately introductory price point.

GEO service pricing across the industry

Standalone GEO retainers vary widely depending on scope:

Full prompt fan-out, digital PR for citation eligibility, multi-platform dashboards

Pricing data synthesizes 2025–26 figures from Brainz Digital, Revv Growth, Sight AI, Digital Elevator, Minuttia, and PageTraffic. Specialized SaaS GEO firms — Skale, Omniscient Digital, Spicy Margarita — bundle GEO into broader content/SEO retainers in the $5,000–$25,000 range.

Practitioner perspectives

Kevin Indig (Growth Memo): "Marketing leaders need to stop funding SEO for clicks and start designing budgets around brand authority in AI-first search."

Jeff Oxford (180 Marketing): "Some merchants are now seeing more conversions from ChatGPT than from traditional Google search. ChatGPT focuses on semantic relevance and draws from multiple sources."

Rosanna Campbell (Backlinko): "Short answer: not yet. But SEO as we know it is dying."

7. Industry sentiment: the bifurcation story

The 2026 data does not support a single narrative. Winners and losers are diverging, often within the same agency segment.

The case that SEO is healthy

Conductor's 2025 State of SEO survey (350 practitioners): 91% reported SEO positively impacted website performance and marketing goals in 2024.

High-maturity enterprises: Conductor found high-SEO-maturity organizations were 3x more likely than average performers to report Google's AIO rollout had a positive impact on traffic.

Market growth: 12–17% CAGR through 2030 across both major forecasting firms.

Search remains dominant: Ahrefs' March 2025 study of 35,000 websites found search drove 43.8% of all web traffic.

Conversion data: Some merchants report AI-referred traffic converts at 4–11x organic search rates (vendor-reported).

The case that the agency business is in distress

SEO job listings were down 37% YoY in Q1 2024 (Search Engine Journal); senior leadership roles (VP/Director SEO) hit hardest.

SparkToro / Rand Fishkin: reported a "bloodbath" of agency owners experiencing their first revenue-declining year in 5+ years.

Holding companies restructuring: GroupM cut nearly half its US headcount; Omnicom merging with IPG; Dentsu targeting 16–17% margins (down from 20–25%); P&G cut 7,000 marketing roles.

SMB retainer compression: Adam Audette reports small-business SEO retainers are 40–50% lower than five years ago.

Agency closures: Wieden+Kennedy India closed October 2024; Havas Creative North America cut 16.7% of staff in 2023 with continued layoffs through 2024–25.

"SEO is dead" check

Per Backlinko: "According to Ahrefs, SEO has died 4,852 times since January 2016."

The 2026 version of the question is sharper than past iterations — because click-economics genuinely shifted, not because Google "died."

What's actually happening: the demand for outcomes (traffic, leads, revenue) is intact and growing. The supply side — generalist agencies competing on rankings — is being restructured.

8. Consolidation & M&A

The SEO tools and media landscape consolidated faster in 2024–26 than in any prior period. The pattern: tools are absorbing media, and big tech is starting to absorb tools.

Date

Acquirer

Target

Significance

Feb 2023

Conductor

Searchmetrics

Enterprise SEO platform consolidation

Nov 2024

Semrush

Search Engine Land

Tools acquire media

Sept 2025

Semrush

Backlinko

Tools acquire content & education

2026 (announced)

Adobe

Semrush

Big tech enters SEO tooling

On the agency side, the equivalent activity is happening more quietly through holdco restructuring, layoffs, and quiet shutdowns. Several mid-tier specialty agencies have been absorbed by larger groups; the public deals are clustered in the tools and media layer.

What this all adds up to

The 2026 SEO agency industry is growing by every market-size measure and bifurcating by every operating measure. Enterprise agencies, niche specialists, and high-maturity in-house teams are gaining share. Generalist mid-market shops competing on rankings are losing it.

Three open questions will define 2026–27:

Will GEO services consolidate into a defined product? The current $937 average AIO add-on is unsustainable; either it becomes a $2,000+ standalone retainer with real deliverables, or it gets absorbed into base SEO retainers at zero marginal price.

Does SMB retainer compression continue? The average $497/month spend may well drop further as AI tools let SMBs DIY more of the work — or stabilize if outcomes-based pricing replaces flat retainers.

Will agency churn improve as AI tooling matures? Agencies that can prove faster results with AI-assisted workflows may pull churn down toward 25%. Agencies that can't may see it cross 50%.

If you want to see how your brand is currently performing across both Google Search Console and AI search platforms (ChatGPT, Claude, Gemini, Perplexity) in a single view — including the gap between where you rank on Google and where you actually get cited by AI — check out QuickSEO at quickseo.ai. It's the data layer most agencies and in-house teams are missing in 2026.

Methodology & caveats

Market-size estimates conflict by 20–30%. The widely repeated $108.28B figure originates from TBRC / Research and Markets methodology, which is broader than Mordor's $83.98B. Both are vendor reports; neither is independently audited. Treat the trend (12–17% CAGR) as more reliable than any specific dollar figure.

Many AI SEO and GEO statistics are vendor-published. Conversion claims like "AI traffic converts 4.4x–23x better than organic" come from agencies selling GEO services. These are directionally consistent but not independently verified — quote with attribution.

Pricing surveys have small samples. SE Ranking surveyed 260 agencies; Ahrefs polled 439. The signal is real but not statistically definitive for the whole industry.

AIO prevalence numbers shift fast. Reported figures range from 13% to 30%+ depending on month, device, query type, and definition. The ~15–25% range is the consensus zone for late 2025.

Sentiment data is qualitative. Multiple "agency owners report tough year" pieces are anecdotal. The hard numbers (37% drop in SEO listings, 38% churn, holdco layoffs) are firmer.

Sources

Primary reports referenced: Conductor State of SEO 2025; Backlinko SEO Statistics 2026 (1,200-business panel); Ahrefs SEO Pricing Study (439 providers); SE Ranking SEO Pricing Survey 2025 (260 agencies); Semrush AI Overviews Study 2025; First Page Sage SEO ROI Statistics 2026; Editorial.link Link Building Survey 2026 (518 SEOs); HubSpot State of Marketing 2026; Pew Research AI Overview CTR study (July 2025); Focus Digital Marketing Agency Churn Report 2026; Mordor Intelligence SEO Services Market 2031 forecast; The Business Research Company SEO Services Market 2026; IBISWorld Industry Report on SEO & Internet Marketing Consultants in the US; seoClarity AI Overviews Impact Report; DemandSage AI SEO Statistics 2026.

Sources and further reading

Verified primary reports and news coverage backing the statistics above, grouped by section.