Google AI Overviews (AIOs) — the Gemini-powered AI summaries that appear at the top of Google's search results page — have become the single most consequential shift in search behavior since the introduction of featured snippets. In under two years, AIOs have moved from limited rollout to a default search surface used by more than 2 billion monthly users, restructuring click-through rates, publisher traffic, citation behavior, and the underlying economics of organic SEO.

This roundup pulls together the most reliable, dated 2025–2026 data from Search Engine Land, Seer Interactive, Ahrefs, Semrush, SE Ranking, BrightEdge, Conductor, SparkToro/Datos, Similarweb, Chartbeat (via Press Gazette and Axios), Pew Research, Profound, Bluefish AI, and Google's own earnings disclosures. It's written for SMB founders, in-house SEOs, and small agencies who need defensible, source-attributed numbers — and a clear distinction between Google AI Overviews (SERP-embedded) and the standalone Gemini chatbot app, which are tracked separately.

A note on conflicting prevalence figures

Before diving in, one caveat: prevalence figures for AI Overviews vary widely across studies because each tracker uses a different keyword set, geography, device mix, and detection method. Reasonable 2026 numbers range from ~21% (Safari Digital, conservative non-branded mix) to ~25% (Conductor's 21.9 million-query benchmark) to ~48% (BrightEdge's 9-industry tracker, March 2026) to 60–65% (Xponent21, AdvancedWebRanking-derived, April 2026). Google's own disclosures (Marketech APAC, February 2026) cite "roughly 50%." Where possible, this report cites the methodology alongside the figure.

1. Market share and prevalence: how often AIOs trigger

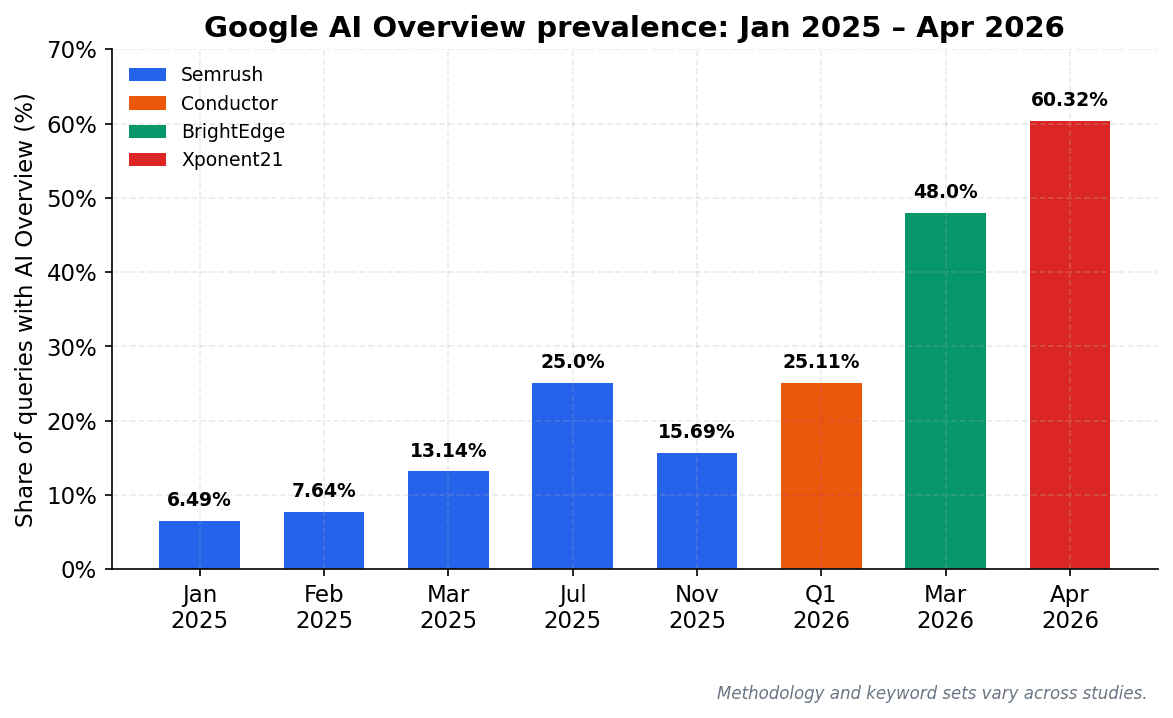

AI Overview prevalence has grown roughly 4–9x in 15 months — but with notable volatility. Semrush data shows AIOs jumped from 6.49% of queries in January 2025 to a peak of about 25% in July 2025, then dropped to 15.69% in November 2025 after Google recalibrated. Conductor's Q1 2026 benchmark across 21.9 million queries put the figure at 25.11%. BrightEdge's 9-industry tracker — focused on commercial verticals — recorded 48% by March 2026, a 58% YoY increase. Xponent21's April 2026 measurement put U.S. AIO prevalence at 60.32%.

The composition of AIO-triggering queries has shifted dramatically. In January 2025, 91.3% of AIO-triggering queries were informational. By October 2025, that had fallen to 57.1% — commercial queries grew to ~19%, and navigational AIO triggers jumped from 0.74% to 10.33%. The implication: AIOs are no longer just a "how does X work" feature. They're now standard for product comparisons, brand searches, and transactional queries — the queries SMBs care about most.

Chart 1: Google AI Overview prevalence trend, January 2025 – April 2026. Methodology and keyword sets vary across studies.

AI Overviews are one surface — ChatGPT is another. See if it cites you with the free ChatGPT rank tracker.

Trigger rate by industry (BrightEdge, Feb 2025 → Feb 2026)

Industry

Feb 2025

Feb 2026

Change

Education

18%

83%

+65 pp

B2B Tech

36%

82%

+46 pp

Restaurants

10%

78%

+68 pp

Healthcare

~30%

75%+

+45 pp

Insurance

~28%

72%+

+44 pp

E-commerce / Shopping

low

3–14%

minimal

Trigger rate by query type (Semrush)

Query type

January 2025

October 2025

Change

Informational

91.3%

57.1%

−34.2 pp

Commercial

~7%

~19%

+12 pp

Navigational

0.74%

10.33%

+9.6 pp

Transactional

low

growing

expanding

Other prevalence patterns worth noting: queries of 8+ words are 7x more likely to trigger an AIO (WordStream); 57.9% of AIO-triggering queries are question-format (Digital Applied); and AIOs occupy roughly 42% of the desktop screen and 48% of mobile, pushing organic results substantially below the fold.

2. User reach and adoption

Google has been consistent in its public disclosures: AI Overviews reach roughly 2 billion users every month. The trajectory has been relentless.

Date

Source

Reach claimed

May 2025 (Google I/O)

Sundar Pichai

1.5B monthly users, 200+ countries, 40+ languages

July 2025 (Q2 earnings)

Sundar Pichai

2 billion monthly users

March 2026

Dan Taylor (VP Global Ads)

2B+ monthly users (post-Gemini 3)

April 29, 2026 (Q1 earnings)

Philipp Schindler (CBO)

"More than 2 billion" — queries at all-time high

Don't conflate AI Overviews with the Gemini app

This is the cleanest distinction quickseo.ai's audience needs to internalize. AI Overviews = the Gemini-powered summaries embedded inside Google Search (~2B monthly users). The Gemini app = the standalone chatbot product, with 750M monthly active users by Q4 2025 (Alphabet earnings) — up from 350M in April 2025. AI Mode = the conversational opt-in mode inside Google Search itself, with 100M+ monthly users in U.S. and India (Q2 2025) and 75M total disclosed by VP of Search Nick Fox in December 2025. We compare all three in detail in Section 6.

3. Click-through rate impact: the floor has been set

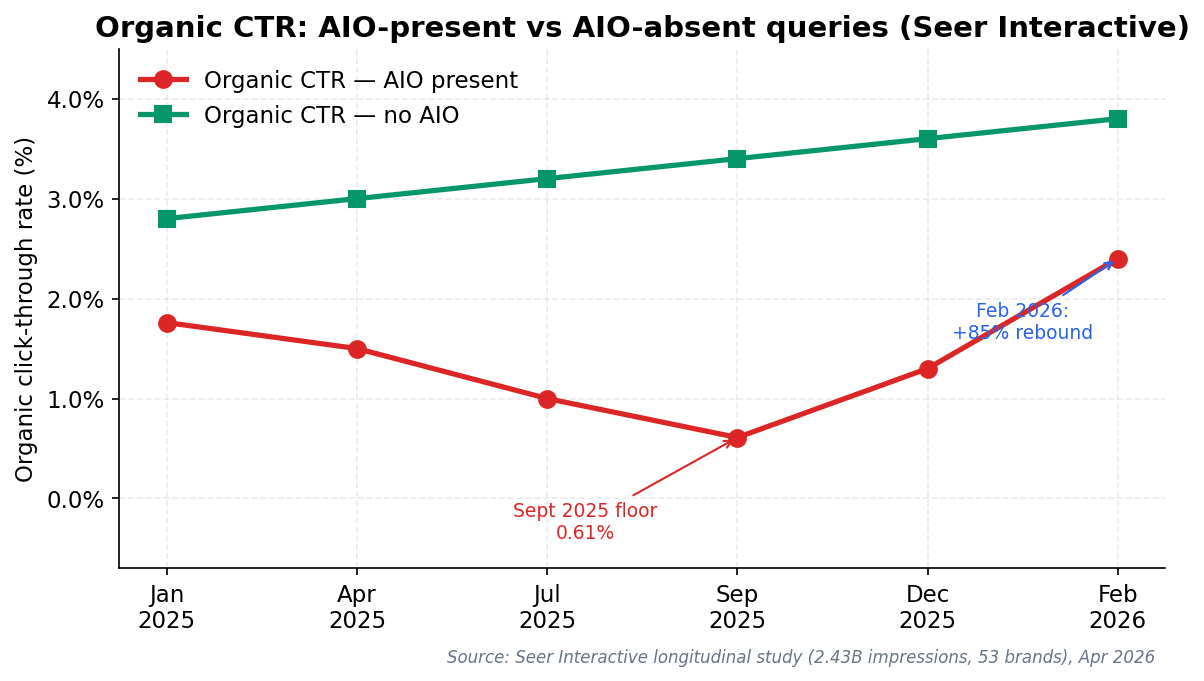

The CTR impact of AI Overviews is the single most-studied AIO question in 2025–2026, and the studies broadly agree on direction (negative) while disagreeing on magnitude. The most important single data point of 2026 is Seer Interactive's longitudinal study, published April 2026 and based on 2.43 billion impressions across 53 brands and 5.47 million queries.

Chart 2: Organic CTR on AIO-present vs AIO-absent queries (Seer Interactive longitudinal study, January 2025 – February 2026).

Three things to take away from the Seer data: (1) organic CTR on AIO queries fell from 1.76% to 0.61% by September 2025 — a 65% collapse; (2) it then rebounded 85% to 2.4% by February 2026; (3) but CTR on queries without an AIO actually rose from 2.8% to 3.8% over the same period. The gap between AIO-present and AIO-absent queries — currently ~37% — is the new normal SEOs need to plan around.

CTR studies side-by-side

Study

Sample size

Headline finding

Date

Seer Interactive

2.43B impressions, 53 brands

−61% then +85% rebound

Apr 2026

Ahrefs

863K keywords / 4M AIO URLs

−58% on top-ranking pages

Dec 2025

Pew Research

900-user clickstream panel

8% click-through with AIO vs 15% without

Mar 2025

Amsive

700K keywords (5 verticals)

−15.5% avg, −27% outside top 3

2025

Daily Mail / DMG

UK desktop monitored set

−89% CTR with AIO present

2025

One nuance often missed: brand presence matters enormously. Per Seer, brands cited inside the AIO get 35% more organic clicks and 91% more paid clicks than non-cited brands on the same SERP. Digital Applied's March 2026 data shows that branded queries with AIOs actually see an 18% CTR increase — strong evidence that AIOs are redistributing clicks toward cited brands rather than uniformly suppressing them.

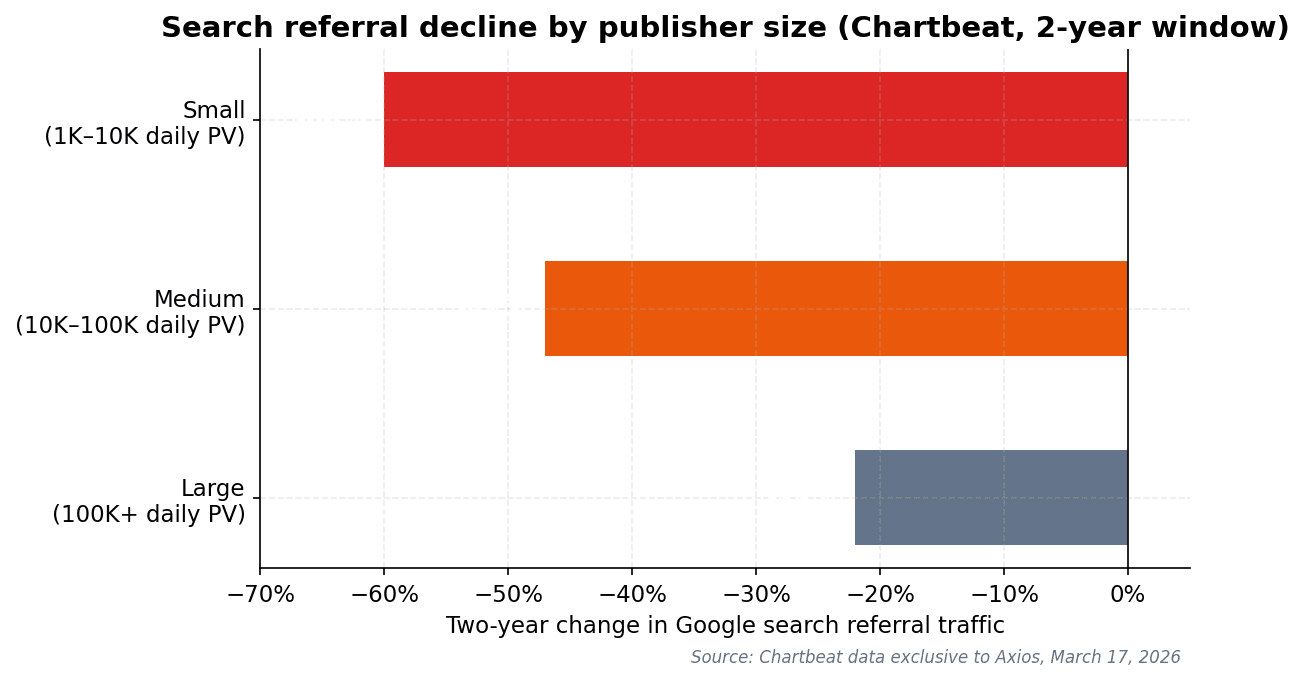

4. Publisher and website traffic decline

Chartbeat's data is the most reliable view of how AI Overviews are reshaping referral traffic, because it spans thousands of publisher sites with consistent measurement. The headline finding from their March 2026 release (exclusive to Axios): smaller sites are getting hit hardest.

Chart 3: Two-year change in Google search referral traffic by publisher size (Chartbeat data, March 2026).

Other key findings from the Reuters Institute / Chartbeat 2026 report (January 13, 2026):

Google search traffic to publishers fell 33% globally in the year to November 2025; U.S. publishers were hit harder at −38%.

Google Discover referrals to 2,500+ publisher sites: −21%.

ChatGPT referrals to publishers grew 200%+ — but still account for less than 1% of all referrals. Chatbot traffic is nowhere near offsetting search declines.

News publisher forecast: −43% search traffic by 2029 (median expectation); ~20% expect declines greater than 75%.

Named publisher disclosures back this up: HubSpot estimates 70–80% organic traffic decline; Business Insider lost 55% from April 2022 to April 2025 (and cut staff by 21%); CNN dropped 27–38%; Chegg's revenue fell 24% YoY and the company sued Google in February 2025 explicitly citing AIO impact.

The financial smoking gun came in Alphabet's Q1 2026 earnings on April 29, 2026: Google Network ad revenue (third-party publishers via AdSense, AdMob, and Ad Manager) fell 4% year-over-year to $6.97 billion — the most direct signal yet that AIO is compressing the open-web economy. Meanwhile Google's owned search revenue grew 19% to $60.4B.

5. Citation behavior — where the GSC-to-AI gap really matters

This section matters most for SMB SEO strategy in 2026. The key insight: citation overlap with the organic top-10 has weakened from ~76% in mid-2025 to between 17% and 54% in early 2026 (depending on study). Ranking #1 no longer guarantees AIO inclusion.

AIOs now contain an average of 13.34 sources per response (up from ~6.82 in 2024) — and 43.42% of AIO responses include links back to Google's own search results pages, typically 4–6 internal links per AIO. That means each AIO is essentially a re-ranked, re-mixed result set drawn from a much wider pool than the visible top-10.

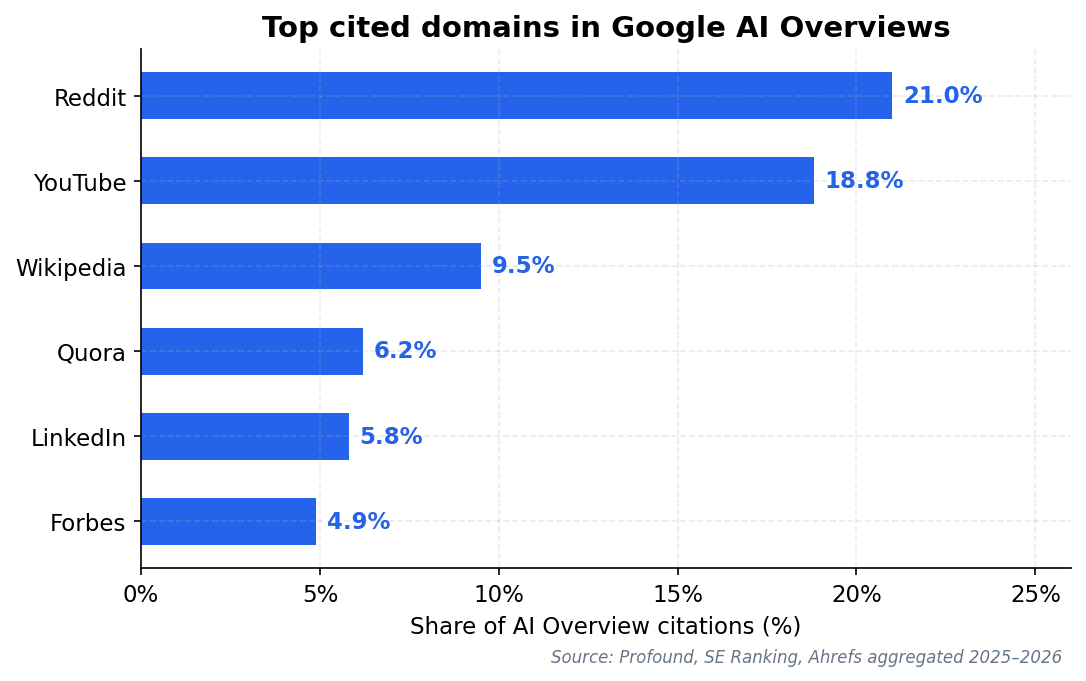

Chart 4: Top cited domains in Google AI Overviews (Profound, SE Ranking, Ahrefs aggregated 2025–2026).

AIO citation – organic overlap over time

Source

Period studied

Top-10 organic overlap

Implication

Ahrefs

Mid-2025

76%

Ranking strongly correlated with AIO inclusion

BrightEdge

May 2024 – Sep 2025

32% → 54.5%

Trend toward greater alignment over 16 months

BrightEdge / ALM

Feb 2026 (post-Gemini 3)

17–38%

Major drop after Jan 27, 2026 model rollout

Citedify

2026 (most bullish read)

93.67%

Methodology dependent — wide range across studies

The citation winners are dominated by community and video platforms. Reddit holds 21% of AIO citations; YouTube has overtaken Reddit as the most-cited source across LLM answers overall (Adweek, January 2026), but Reddit still leads inside Google AI Overviews specifically. LinkedIn is the most-cited domain for professional and B2B queries across AIOs, AI Mode, ChatGPT, Copilot, and Perplexity (Profound, March 2026). For software queries, G2 is the dominant review platform in AIOs (Radix, 2026).

This is the heart of the problem traditional SEO tools weren't built for: Google Search Console shows you which queries trigger your impressions and clicks, but it doesn't tell you whether you're cited inside the AIO box. Ahrefs and Semrush show your rank, but ranking #1 only gives you a 17–54% chance of AIO inclusion in 2026. The gap between the two layers is now its own metric — and one that needs its own tracking.

6. AI Overviews vs AI Mode vs the Gemini app

These three surfaces all use Gemini, all carry Google branding, and are constantly conflated in industry coverage. They behave very differently — and need to be tracked separately.

Surface

What it is

2026 reach

How to track

Google AI Overviews

Gemini-powered summaries embedded at the top of Google Search results

2B+ monthly users in 200+ countries

SERP feature trackers in Ahrefs/Semrush/SE Ranking; manual SERP testing

AI Mode

Conversational opt-in mode inside Google Search

100M+ MAU U.S./India; 75M total (Dec 2025); 1B+ monthly queries

SE Ranking AI Mode tracker; Profound; Bluefish; Datos

Gemini app

Standalone Gemini chatbot (gemini.google.com)

750M MAU (Q4 2025); 1.1B monthly visits

Direct LLM citation trackers (Profound, BrandRank.AI, Otterly, Superlines)

Gemini API / Workspace

Developer & enterprise distribution

85B API requests/month (+142% YoY); 8M+ Gemini Enterprise seats

API usage dashboards

Other useful contrasts: AIO sessions average about 21 seconds of user time per query (Growth Memo); AI Mode averages 49 seconds — and 77 seconds for brand-comparison queries. Zero-click rates: 83% with AIO vs 93% in AI Mode (Seer Interactive). And in AI Mode, only 14% of cited URLs rank in Google's top 10 (SE Ranking) — compared to 17–54% for AIOs. The further you move toward conversational AI, the less traditional ranking matters.

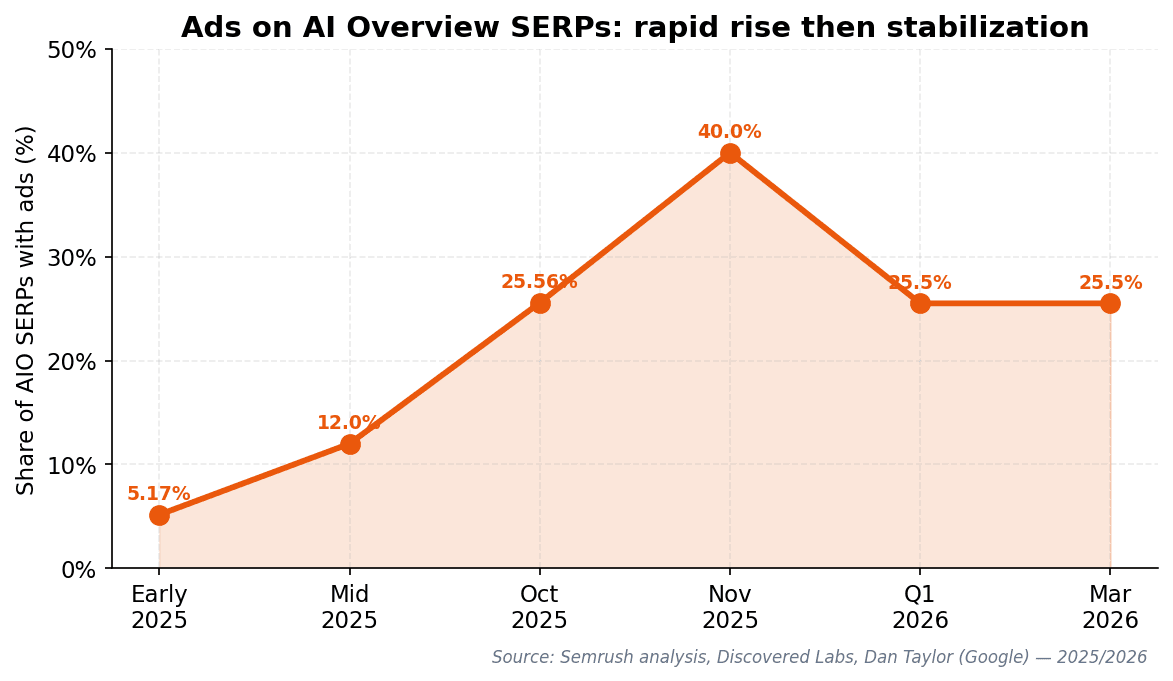

7. Ads in AI Overviews: 2026's quiet revolution

The rise of ads inside AIO SERPs is one of the most underreported stories of 2026 and has direct bearing on paid-search strategy.

Chart 5: Share of AIO SERPs containing ads, 2024–2026 (Semrush, Discovered Labs, Google disclosures).

As of January 2026, ads in AIOs appear above and below the AI-generated summary in traditional SERP slots — the AI-generated text itself remains ad-free (Discovered Labs, January 2026). Google has confirmed work on "Direct Offers," an AI Mode pilot ad format that surfaces personalized deals at high purchase intent, with broader rollout targeted for 2026.

Per Seer Interactive's April 2026 update: paid CTR with AIO present rose slightly from 14.6% to 16.2% in Q1 2026, while paid CTR without AIO fell from 26% to 21.8%. Paid clicks are migrating toward AIO-present SERPs. eMarketer forecasts U.S. AI search ad spend to grow from $2.08B in 2026 to $25.93B by 2029 — from 1.3% to 13.6% of total search ad spending.

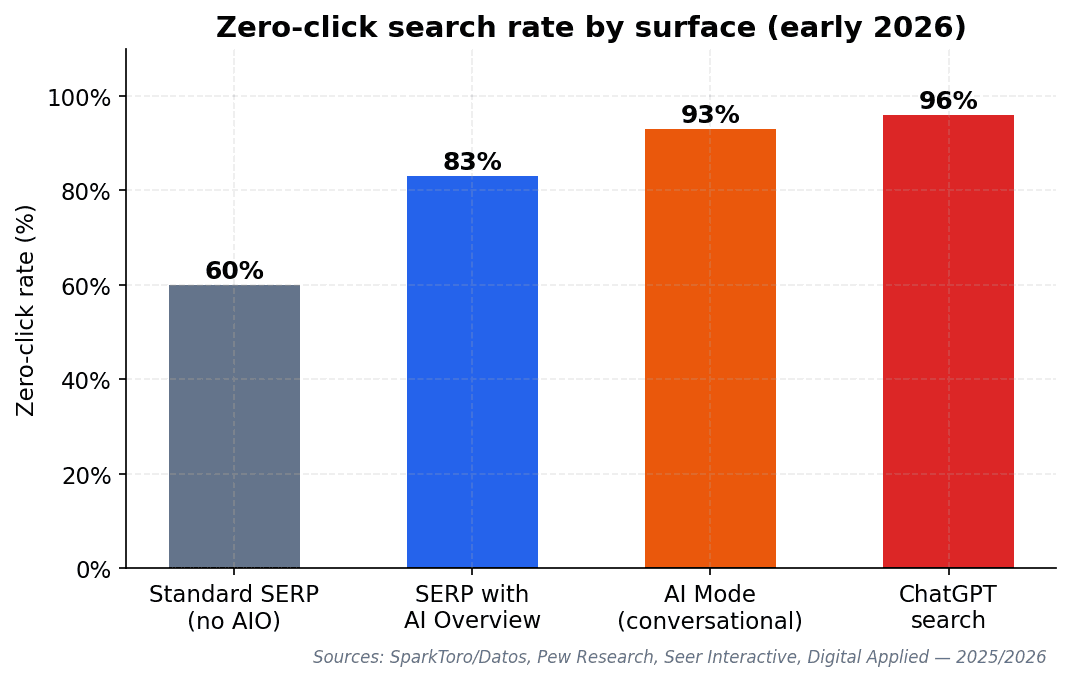

8. Zero-click search rate

Zero-click search has been climbing for years, but AIOs represent a step-change. The contrast across surfaces is sharp:

Chart 6: Zero-click search rate by surface in early 2026 (SparkToro/Datos, Pew Research, Seer Interactive, Digital Applied).

Pew Research's March 2025 panel found that 26% of AIO-present sessions end the search entirely (vs. 16% for non-AIO sessions). AIOs don't just suppress clicks — they end search journeys earlier.

One counterpoint worth flagging: Datos's Q1 2026 State of Search report (April 27, 2026) found that U.S. zero-click rate actually fell from 24.5% in December 2025 to 22.4% in March 2026 (using a strict clickstream methodology). The two figures aren't directly comparable to SparkToro's older keyword-level analysis, but Datos's panel suggests zero-click pressure may be leveling off as AIO prevalence stabilizes — supporting the broader thesis that we've passed the worst of the 2025 disruption.

9. Google AI Overviews in context: vs ChatGPT, Perplexity, Claude, Grok

Standalone AI search platforms get most of the press, but Google AI Overviews dwarf them all in raw reach because they're embedded in a product (Google Search) with near-universal adoption.

Platform

Monthly reach (early 2026)

AI referral traffic share

Google AI Overviews

2B+ MAU (within Google Search)

(measured inside Google)

ChatGPT

800M WAU / ~400M MAU; 2.5B queries/day

87.4%

Gemini app (standalone)

750M MAU; 1.1B monthly visits

~8%

Microsoft Copilot

13.2% AI chatbot share

minor

Perplexity

22M MAU; 780M monthly queries

2–3%

Claude

~19M MAU; ~190% YoY growth

<2%

Grok (xAI)

29.6M visits (July 2025); ~3.4% share

~2.5%

Bottom line: Google AI Overviews reach roughly 2.5x more users than ChatGPT and 4x+ more than the entire rest of the AI chatbot market combined. No standalone AI tool can replicate this distribution, which is why AIO impact dwarfs standalone-AI impact for most SMBs and publishers today. That said, AI referral traffic from chatbots converts at 14.2% on average vs. Google organic at 2.8% (Exposure Ninja synthesis) — fewer visits, dramatically higher intent.

10. What this means for SMBs and small agencies

The 2026 data tells a consistent story. Five takeaways worth internalizing:

CTR has stabilized but at a permanently lower floor. Seer's April 2026 rebound shows we've passed the worst, but the gap between AIO-present and AIO-absent CTR (~37%) is the new baseline. Plan capacity, content investment, and forecasts around this — not around 2024 numbers.

Citation matters more than ranking. Brands cited inside an AIO get 35% more organic clicks and 91% more paid clicks. Citation overlap with organic top-10 has weakened from ~76% to 17–54% — meaning rank tracking alone misses the layer that drives outcomes. AI visibility tracking is now table stakes, not nice-to-have.

Small publishers and small DTC brands are most exposed. Chartbeat's data is unambiguous: smaller sites lost 60% of search referrals in two years vs. 22% for large publishers. Brand recognition, direct/email channels, and presence on YouTube, LinkedIn, and Reddit are now structural defenses.

Industry exposure is highly uneven. Education, B2B Tech, Restaurants, Healthcare, and Insurance face 75–83% AIO trigger rates. E-commerce queries remain relatively protected (3–14%) — but ads on AIO SERPs and the rise of ChatGPT Instant Checkout are starting to encroach on commercial intent everywhere.

The Gemini-3 rollout in January 2026 may have permanently decoupled ranking from AIO inclusion. If the post-rollout drop in top-10 overlap holds, the SEO playbook bifurcates: traditional ranking work + multi-platform brand presence (YouTube, Reddit, LinkedIn, G2) + LLM-readable structured content. Brands operationalizing this two-layer model are the ones the data shows are absorbing — rather than losing — the AI search transition.

The missing piece: where traditional SEO tools fall short

Here's the practical gap every SMB SEO is now running into. Google Search Console shows you which queries triggered your impressions and clicks, and how that's trending — but it doesn't tell you which of those queries triggered an AIO, whether you were cited inside it, or how that compares to the same brand searches on ChatGPT, Claude, Gemini, or Perplexity. Ahrefs and Semrush show your rank — but ranking #1 only gives you a 17–54% chance of AIO inclusion in 2026, and zero visibility into AI-only platforms.

This is why we built QuickSEO — to give SMB founders, in-house SEOs, and small agencies a single view that bridges traditional GSC data with AI visibility tracking across ChatGPT, Claude, Gemini, AI Overviews, and Perplexity.

Sources and methodology

Every statistic in this post is dated and sourced. Primary sources used: