ChatGPT hit 900 million weekly active users in February 2026 — yet its share of US mobile chatbot DAU collapsed from 69.1% to 38.7% in just 14 months (Fortune / Apptopia, Apptopia data brief). Both numbers are true at the same time, and that's the whole story of the 2026 chatbot market: the category is getting bigger, ChatGPT is still on top, and every challenger is winning a different slice.

This isn't a ranking — it's a scoreboard. ChatGPT has the consumer audience. Gemini has the distribution. Claude has the enterprise. Perplexity has the citation depth. Below are 40+ vetted 2026 stats on each, with side-by-side comparisons where the data exists.

One methodology note up top: chatbot market share depends entirely on the panel. Statcounter measures worldwide web traffic. FirstPageSage measures US blended share. Similarweb measures web visits. Apptopia measures US mobile DAU. ChatGPT's share reads 76.85% on one panel and 38.7% on another — same quarter. Every chart in this post is labelled with its source so you know which lens it represents.

The 2026 chatbot scoreboard at a glance

Each column is the leader on something different. Read the rows, not just the headline.

Metric

ChatGPT

Gemini

Claude

Perplexity

Monthly active users

~1B est.

750M

~18.9M

45M

Weekly active users

900M

—

—

—

Monthly visits (Mar 2026)

5.73B

~930M

613.7M

~170M

Daily queries

2.5B+

—

—

30–45M

Latest revenue / ARR

$25B (Feb '26)

Part of >$400B Alphabet

$30B run-rate (Apr '26)

$200–450M

Latest valuation

$852B (Mar '26)

—

$380B (Feb '26)

$20B (Sept '25)

US chatbot share (May '26)

60.6%

15.1%

5.0%

5.4%

Avg session (Similarweb)

5:52

7:11

5:56

4:48

US mobile DAU share (Mar '26)

38.7%

~25%

~10%

2.1%

Sources: OpenAI press / TechCrunch, Alphabet Q4 2025 earnings, Anthropic announcements, Perplexity disclosures, Similarweb, FirstPageSage, Apptopia. ARR figures are mix of disclosed and analyst estimates.

Scale: ChatGPT is the only one with nine-figure WAU

OpenAI disclosed 900 million weekly active users on February 27, 2026 — more than doubling from 400M in February 2025 (TechCrunch — 900M WAU). The growth ladder: 400M (Feb 2025) → 700M (Sept 2025) → 800M (Oct 2025) → 900M (Feb 2026). Industry estimates put daily active users around 210M, roughly 23% of WAU.

Traffic backs the headline. Similarweb clocks 5.35 billion visits to chatgpt.com in February 2026 and 5.73 billion in March — the fifth-highest monthly traffic in the product's history. The US drives 18.86% of visits; India is the fastest-growing top-five market at 9.76%.

Query volume is the strongest signal of all. OpenAI disclosed 2.5 billion daily user prompts on July 21, 2025 — ~29,000 per second (TechCrunch — 2.5B prompts/day). For comparison, Google handles ~14B searches a day, which means ChatGPT is already at ~18% of Google's daily query volume. The 2.5B figure has not been updated publicly since; current run-rate is almost certainly higher.

On mobile, ChatGPT was Apple's #1 most-downloaded US app of 2025 (up from #4 in 2024), and overtook TikTok as the #1 free app worldwide on iOS and Android in March 2026 (TechCrunch — Apple App Store 2025). Total app downloads for 2025: ~770M.

Revenue is finally catching up to the audience. OpenAI's CFO Sarah Friar confirmed $20B ARR at the end of 2025; Sacra estimates $25B annualized by February 2026; OpenAI's March 2026 funding announcement disclosed $2B/month revenue. The same announcement closed a $122B raise (Amazon $50B, Nvidia $30B, SoftBank $30B) at an $852B post-money valuation (OpenAI — accelerating the next phase of AI). Paying customers: 50M+ consumer subscribers and 9M+ business users.

Usage is broader than coders. OpenAI's economic-research paper found that ~80% of ChatGPT usage falls into three buckets — Practical Guidance, Seeking Information, and Writing — and the split is 70% personal / 30% work (OpenAI / NBER WP w34255). Coding is only 4.2% of ChatGPT messages, versus ~35% on Claude — a remarkably clean split that explains why Anthropic's enterprise numbers look so different in §4.

ChatGPT's scale is also why how ChatGPT stacks up against Google Search is now the most-asked question in SEO. The 2.5B-prompts/day number has crossed enough threshold that ChatGPT is competing for the same intent that Google has owned for 25 years.

Growth: Gemini is the breakout #2

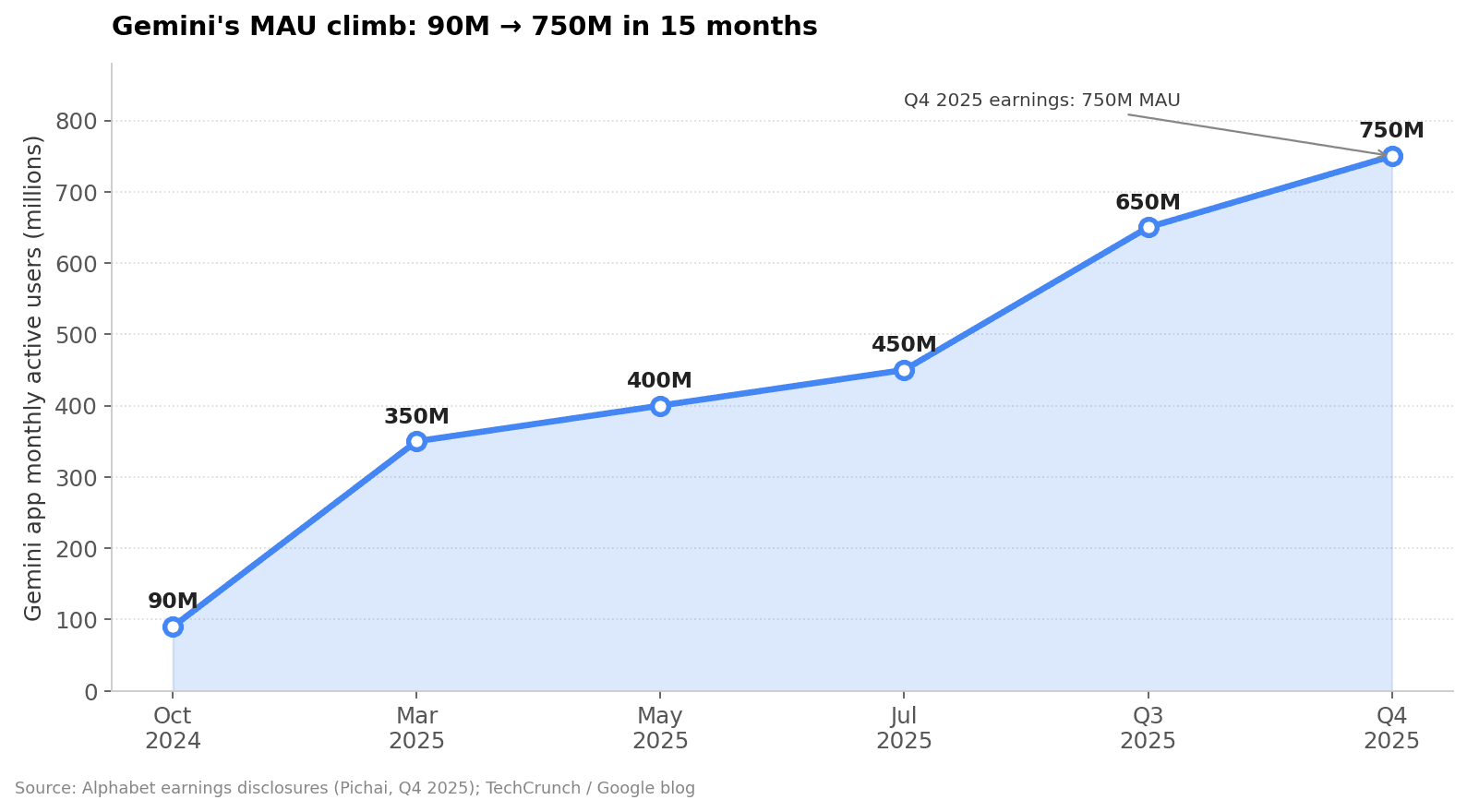

Sundar Pichai disclosed 750 million Gemini app MAU in the Q4 2025 earnings call on February 4, 2026 — more than double the 350M from March 2025 (Alphabet Q4 2025 earnings — CEO remarks). The growth ladder is steeper than ChatGPT's: 90M (Oct 2024) → 350M → 400M → 450M → 650M → 750M in 15 months.

Gemini app MAU disclosed across four Alphabet earnings calls. Source: Pichai CEO remarks, Q4 2025 earnings; TechCrunch.

That's just the standalone app. The Gemini-powered AI Overviews surface in Google Search reached 2 billion monthly users in 200 countries (Q2 2025), and AI Mode hit 75M daily users worldwide by early 2026 (TechCrunch — Q2 2025 metrics, Search Engine Journal — AI Mode 75M DAU). No other chatbot has distribution like that.

API volume tells the same story. Gemini processes 10 billion+ tokens per minute via direct API as of Q4 2025 (up from 7B in Q3); monthly tokens processed crossed 980 trillion in July 2025 and Gemini 3 Pro processes 3× the daily tokens that Gemini 2.5 Pro did. Serving unit cost is down 78% in 2025.

Workspace distribution is the quiet weapon. 8 million paid Gemini Enterprise seats sold in the first four months after launch. 95% of the top 20 SaaS companies and 80%+ of the top 100 SaaS companies use Gemini. 13M developers building with the API. 110M Google Meet attendees used "Take Notes For Me" in the last month tracked — that one Gemini feature alone has more monthly users than Claude has total. And in 2026 Gemini is fully replacing Google Assistant on Android.

Gemini 3 launched November 18, 2025 — Pichai called it the "fastest adoption of any model in our history." Gemini 3.1 Pro followed February 19, 2026. Google AI Plus, a $7.99/month consumer subscription, launched in January 2026 as a cheaper entry point than the existing Pro/Ultra tiers.

Enterprise: Claude owns the API spend

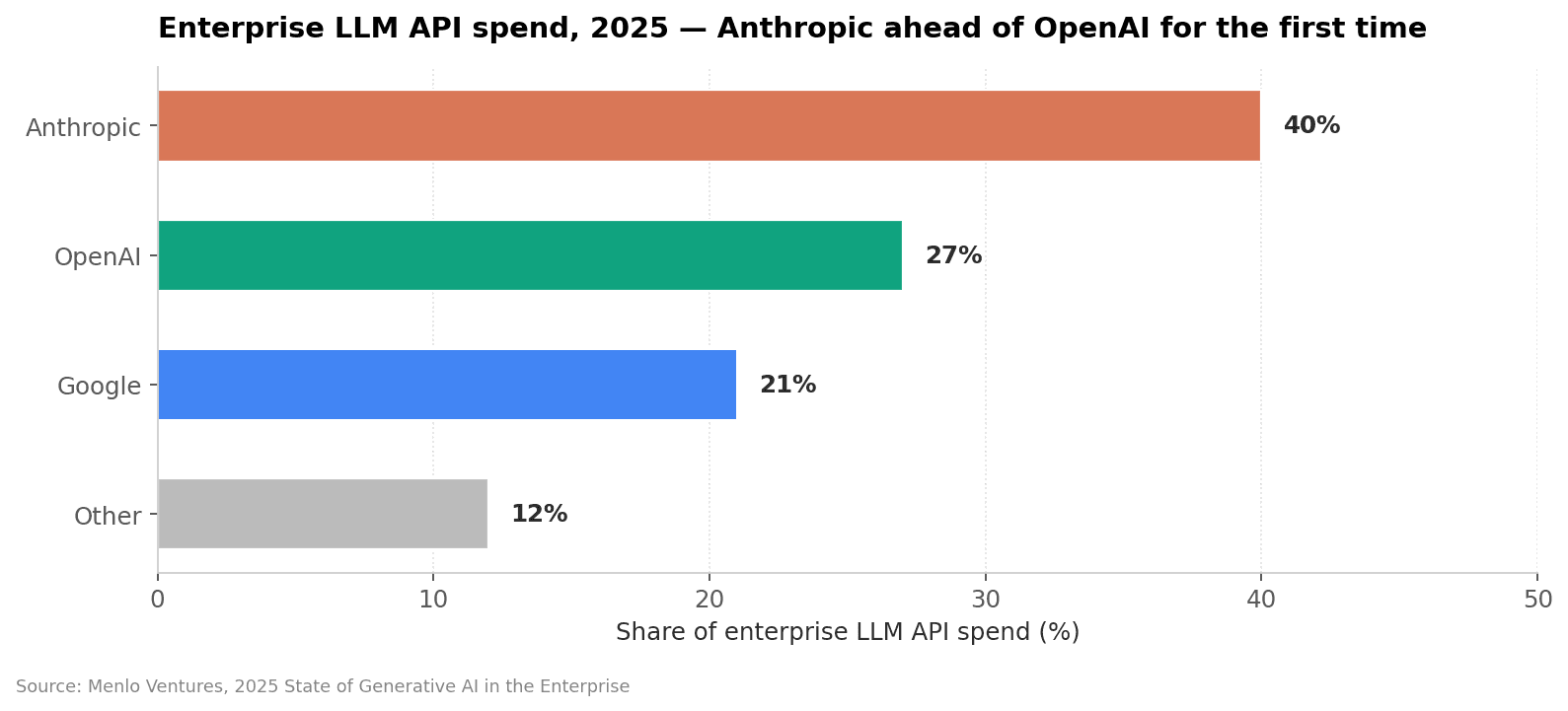

Menlo Ventures' 2025 State of Generative AI in the Enterprise is the cleanest read on enterprise LLM spend, and the numbers are stark: Anthropic now captures 40% of enterprise LLM API spend, up from 12% in 2023. OpenAI fell from 50% to 27% over the same window. Google is at 21%.

Source: Menlo Ventures 2025 State of Generative AI in the Enterprise. "Other" includes Mistral, Cohere, Meta, and long-tail vendors.

The behavioral data lines up. Anthropic wins ~70% of enterprise head-to-head bake-offs against OpenAI when buyers choose for the first time. The coding LLM market is a $4B category that Anthropic has dominated for 18 months straight.

Revenue confirms it. Anthropic's annualized run-rate hit $30 billion in April 2026 — 80× growth in 16 months (VentureBeat — Anthropic $30B ARR). The full trajectory: $87M (Jan 2024) → $1B (Dec 2024) → $9B (end 2025) → $14B (Feb 2026) → $19B (March 2026) → $30B (April 2026). Claude Code alone hit $2.5B run-rate by February 2026 — the fastest product ramp in enterprise software history. 80% of Anthropic revenue comes from business customers, the inverse of OpenAI's consumer-heavy mix.

Big customers, lots of them. 1,000+ enterprise customers spending $1M+/year as of April 2026 — doubled from 500 in under two months since the Series G closed. 8 of the Fortune 10 and ~70% of the Fortune 100 are paying Claude customers. Anthropic announced enterprise wins at Salesforce, Palo Alto Networks, Cox Automotive, Novo Nordisk, Nordea, IG Group, Allianz, and Accenture in the last six months alone.

Funding has tracked the revenue. Series G in February 2026 raised $30 billion at a $380B post-money valuation, led by GIC and Coatue (Anthropic — Series G announcement). Two months later Google announced an additional commitment of up to $40 billion ($10B cash + $30B contingent + 5GW compute, April 24, 2026) — and Amazon and Anthropic struck a separate $100B compute deal for up to 5GW. VC offers valuing Anthropic at $800B+ are reportedly circulating.

Consumer Claude is suddenly waking up too. Claude.ai visits are up ~5× year-over-year to 1.08B in Q1 2026; 613.7M visits in March 2026 alone. 74.4% of claude.ai desktop traffic is direct — a brand-driven demand signal you don't see on most AI sites. Most strikingly, Apptopia reported that in March 2026 Claude overtook ChatGPT as the most-downloaded AI app in the US (149K daily downloads vs ChatGPT's 124K). Mobile DAU share went from under 2% in December 2025 to ~10% in March 2026.

Models shipped in the last eight months: Sonnet 4.5 (Sept 29, 2025), Haiku 4.5 (Oct 15), Opus 4.5 (Nov), Sonnet 4.6 (Feb 17, 2026), Opus 4.7 (April 2026). 46% of developers name Claude Code their "most loved" tool, versus Cursor 19% and GitHub Copilot 9% — and 70–90% of code shipped by Anthropic's own engineering teams is produced by Claude Code.

Citation depth: Perplexity is the answer-engine specialist

Perplexity is the smallest of the four by audience — ~45 million MAU in late 2025/early 2026, up from 22M at the start of 2025 — but it's the leader on the metric brands actually care about: how many sources it cites per answer.

BrightEdge measures an average of 8.79 citations per Perplexity response, and Superlines puts Perplexity's citation rate at 15.43% versus ChatGPT's 2.78% — meaning Perplexity is roughly 5.5× more likely to cite a source it pulled from. The product retrieves 60+ sources per query and cites 3–4 of the ~10 pages it actually visits.

Query volume is climbing too. Aravind Srinivas disclosed 780 million queries in May 2025 with >20% month-over-month growth at the time (Just Think AI — Srinivas / 780M queries). Estimates put 2026 run-rate at 1.2–1.5 billion monthly queries, or 35–45M per day. The internal target is 1 billion weekly queries.

Distribution is the most aggressive of any chatbot on this list. The Comet browser went macOS/Windows (July 2025) → Android (November 2025) → iOS (March 18, 2026) and ranked #3 on the US iOS App Store at launch with 100K+ US downloads in the first wave (MacRumors — Comet on iPhone). Comet became free globally in October 2025 (it had been a $200/month Max-only feature) and partnerships with SoftBank and Deutsche Telekom bundle 12 months free Perplexity Pro to a combined ~335 million telco subscribers. The Deutsche Telekom "AI Phone," co-built with Perplexity at a sub-$1,000 price point, ships in 2026.

Business model also flipped. Perplexity shut down its ad business in February 2026 and pivoted to a subscription-first model. ARR was ~$80M end-2024 → $200M end-2025 (Sacra) → reportedly $450M by March 2026; the 2026 target is $656M. Last priced round: $20B (September 2025); lifetime funding $1.5B+. The smallest revenue but the cleanest user-source loop of the four.

Market share, four ways (and why the headlines disagree)

Pick any chatbot, pick any quarter — you can get any market-share number you want depending on the panel. Here's the same Q1/Q2 2026 window through four different lenses:

Platform

Statcounter (Apr '26, global web)

FirstPageSage (May '26, US blended)

Similarweb (Jan '26, US web)

Apptopia (Mar '26, US mobile DAU)

ChatGPT

76.85%

60.6%

68%

38.7%

Gemini

9.00%

15.1%

18.2%

~25%

Claude

2.66%

5.0%

2%

~10%

Perplexity

7.73%

5.4%

2%

2.1%

Copilot

3.76%

12.5%

1.2%

~10%

Grok

—

0.6%

2.9%

13.5%

All four readings come from Q1/Q2 2026. None of them agree, because they measure different things — global web traffic vs US blended vs US web vs US mobile DAU. Sources: Statcounter, FirstPageSage, Similarweb, Apptopia.

ChatGPT looks anywhere from totally dominant (76.85% on Statcounter's worldwide web panel) to a minority (38.7% on Apptopia's US mobile DAU panel). Both are real. Same chatbot, same quarter — different definitions of "share."

Three practical implications for anyone trying to track this:

Don't compare market-share quotes across sources without checking the methodology. Statcounter and Apptopia disagree because one is web traffic and the other is mobile DAU, not because one is wrong.

For consumer reach, mobile DAU is the most honest panel. ChatGPT below 40% on Apptopia in March 2026 is the cleanest signal that the consumer competitive landscape is finally splitting open.

For brand visibility, none of these panels are the right metric. Citation share — what fraction of all AI-chatbot referrals went to your site — is the brand-relevant number (see §8).

Mobile: ChatGPT's share is sliding fast

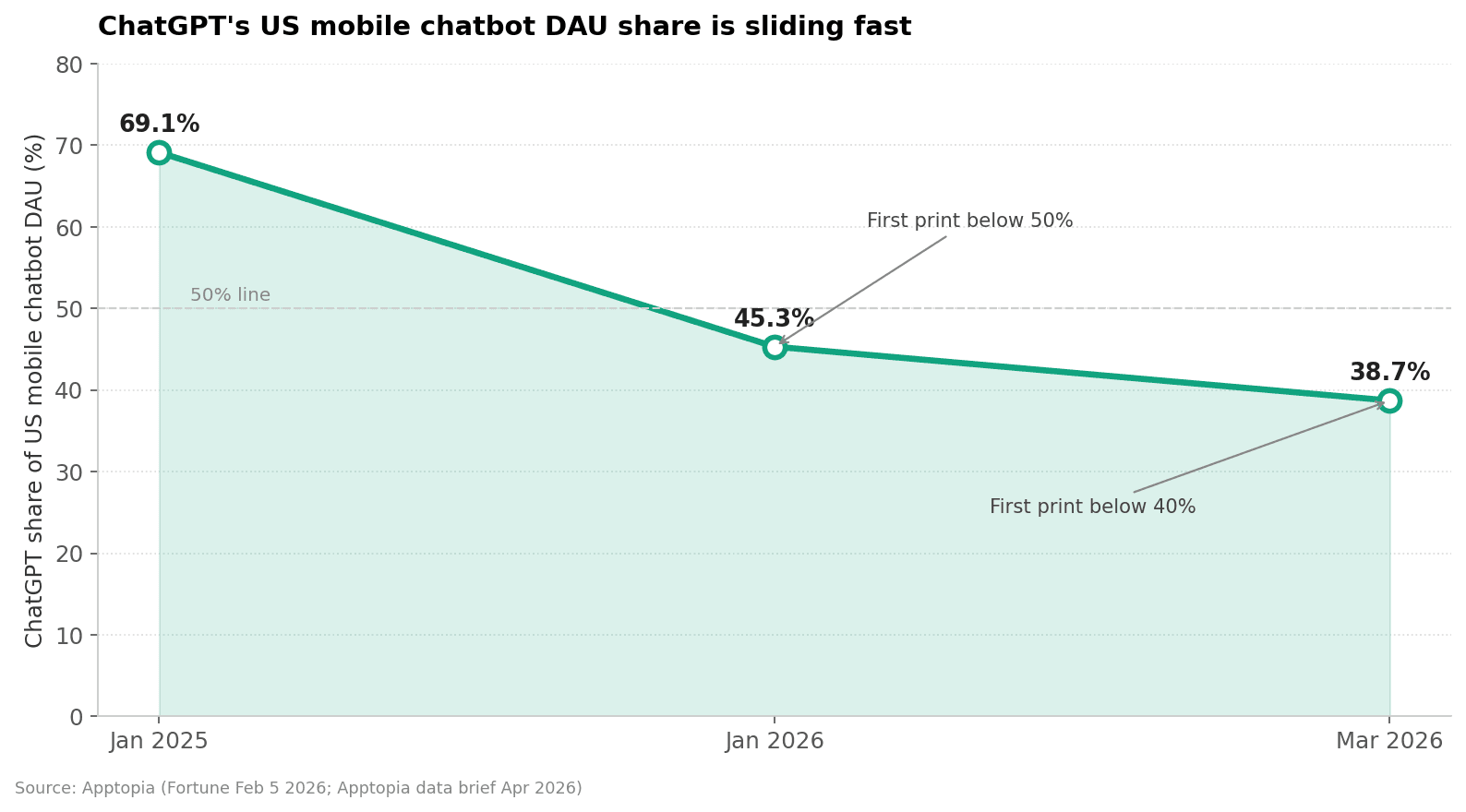

The mobile chatbot category was effectively a ChatGPT monopoly twelve months ago. It isn't anymore. ChatGPT's share of US mobile chatbot DAU fell from 69.1% in January 2025 to 45.3% by January 2026 — the first time below 50% — then to 38.7% by March 2026 — the first time below 40% (Apptopia — Gen AI Chatbots brief, April 2026).

ChatGPT's US mobile chatbot DAU share, January 2025 – March 2026. Source: Apptopia (via Fortune Feb 5, 2026 and Apptopia data brief April 2026).

The pie expanded faster than ChatGPT lost share — overall mobile gen-AI app revenue hit $3 billion in 2025 (+273% YoY), with downloads up 178%. ChatGPT is shrinking in share, not in absolute usage. The category just grew around it.

Who picked up the slack? The fastest-growing app of 2025–26 by a wide margin is Grok: US mobile chatbot share went from 1.6% to 17.8% YoY (Apptopia/Reuters, January 2026) thanks to X integration. Gemini moved from 14.7% to ~25% over the same window. Claude went from under 2% in December 2025 to ~10% in March 2026 — a 167% MoM jump in downloads in March alone.

Engagement varies more than share. Average Similarweb session times across the AI-chatbots category (April 2026): Grok 10:59, Gemini 7:11, Claude 5:56, ChatGPT 5:52, Perplexity 4:48, Copilot 4:09. Claude power users — who skew engineering — average 139 minutes per day in-app.

Citation share: the only metric that matters for brands

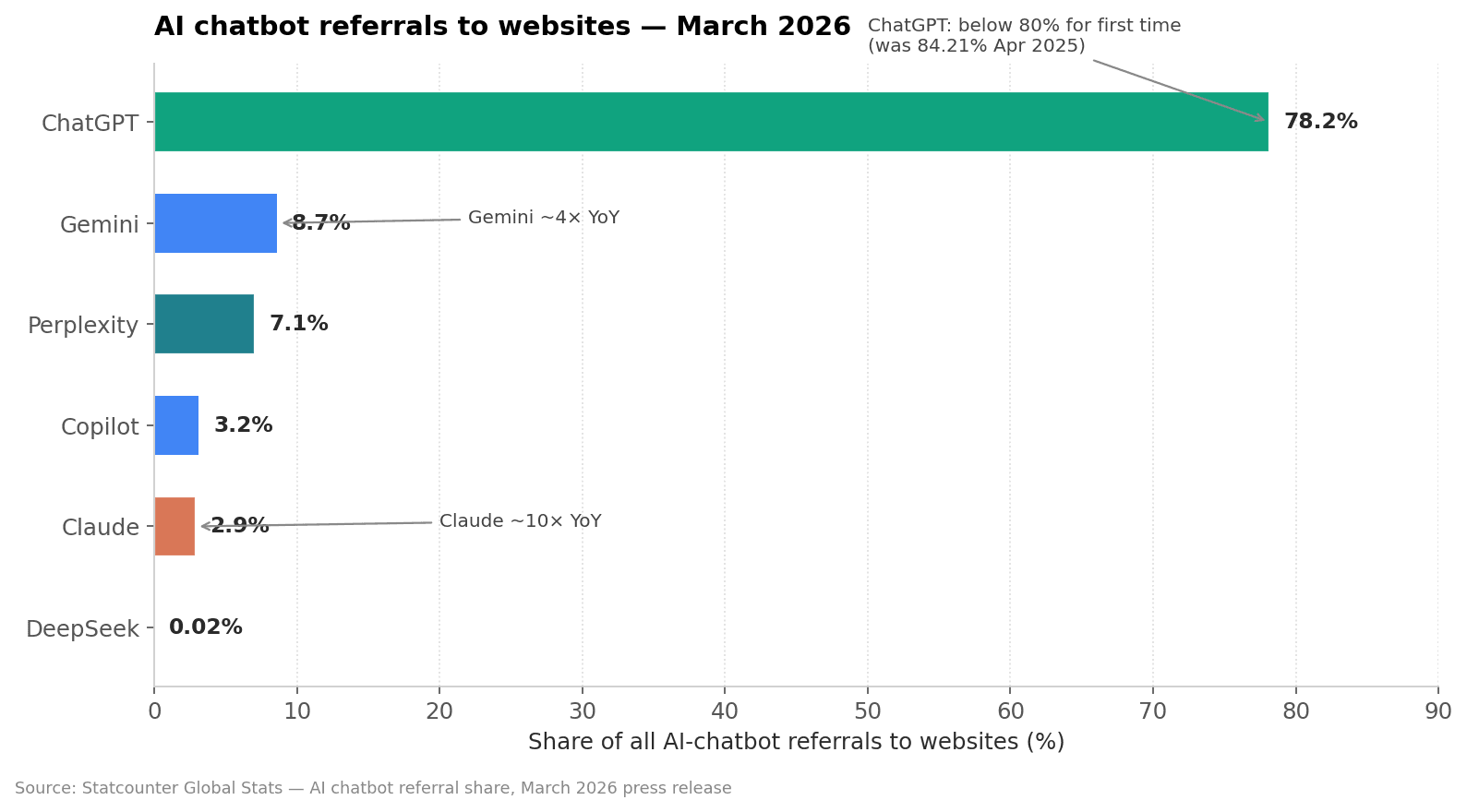

Raw mobile DAU doesn't help if a chatbot never sends users anywhere. The brand-relevant question is: when an AI chatbot answers, does it cite you, and how often? Statcounter's AI chatbot referral share panel — which measures the fraction of all outbound AI-chatbot referrals that go to websites — is the cleanest read.

Share of all AI-chatbot referrals to websites, March 2026. Source: Statcounter Global Stats. ChatGPT below 80% for the first time; Gemini ~4× YoY; Claude ~10× YoY.

ChatGPT crossed below 80% of all AI-chatbot referrals for the first time in March 2026 (78.16%, down from 84.21% in April 2025). Gemini took #2 from Perplexity in late 2025 and now sits at 8.65% (up from 2.31% a year earlier). Claude's referral share grew ~10× year-over-year — peaking at 3.6% in mid-March 2026 before settling at 2.91%.

What each chatbot pulls from looks completely different. The 5W Citation Source Index 2026 analyzed 680 million citations across the major AI platforms (5W — AI Platform Citation Source Index 2026). The headline source-mix split:

ChatGPT: Wikipedia + encyclopedic content account for 47.9% of top citations

Perplexity: Reddit alone is 46.7% of citations

Google AI Overviews: YouTube and multi-modal sources = 23.3% of citations

Domain overlap: Only 11% of top citations are shared between ChatGPT and Perplexity. The two platforms effectively read different webs.

Concentration: Top 15 domains account for 68% of all AI citation share — citations are wildly head-heavy.

If you want to dig into the per-platform source-mix split — and what it implies for the kinds of pages each chatbot likes to cite — we've written a deeper breakdown of what each chatbot actually cites across ChatGPT, Claude, Gemini, and Perplexity.

The variance gets dramatic at the brand level. Superlines tracked a single brand across the major chatbots in March 2026 and measured a 615× citation-volume gap between Grok and Claude on the same brand-related queries — brand-mention rates vary by orders of magnitude across platforms, which is precisely why single-chatbot tracking misleads.

The combined picture: 1B+ users, heavy multi-tenanting

DataReportal's Digital 2026 report puts the global standalone-AI-tool monthly user count at 1 billion+ — and that excludes embedded chatbots like Meta AI (1B MAU but mostly inside Facebook/Instagram/WhatsApp), Snapchat's My AI, Copilot inside Microsoft 365, and the dozens of AI features embedded in Notion, Linear, and the like.

AI platform visits grew 28.6% in the US between January 2025 and January 2026 (Similarweb). AI Overviews now trigger on 48% of tracked Google queries (BrightEdge Feb 2026, up 58% YoY) — and only 38% of the pages cited in those AI Overviews also rank in the organic top 10 (Ahrefs), down from 76% seven months earlier. The chatbot category is no longer a sidecar to search; it's eating the SERP.

Multi-tenanting is the underrated stat. Similarweb cross-panel data shows ~20% of ChatGPT weekly web users also use Gemini, and a striking 79% of OpenAI's paying customers also pay for Anthropic. Users aren't picking one chatbot — they're using two or three. Tracking just one means missing 60–80% of the picture for the typical buyer.

What this means if you market a brand online

Three takeaways from the data above:

There is no single "the chatbot that matters" in 2026. ChatGPT has consumer reach, Gemini has search distribution, Claude has the enterprise, Perplexity has the citation depth. Whoever you're trying to reach lives on more than one platform.

Don't compare market-share numbers across sources without checking the methodology. The same quarter can read 76.85% (Statcounter, global web) or 38.7% (Apptopia, US mobile DAU) for the same product.

Track citation share, not raw market share. With 615× variance in brand-mention rates across platforms, single-chatbot tracking is the modern equivalent of optimizing only for Bing.

Track your visibility across all four chatbots

If your AI visibility dashboard only covers one chatbot — or if you don't have one yet — you're missing 60–80% of how your brand is showing up. QuickSEO tracks how often your brand is mentioned and cited across ChatGPT, Gemini, Claude, and Perplexity alongside Google Search, so you can see exactly which platforms are surfacing you, which prompts trigger competitors instead, and where your category share is moving. Run a free AI visibility audit on your domain — no credit card required.

The bottom line

2026 is the first year there's no consensus winner of the chatbot category. ChatGPT has the audience. Gemini has the distribution. Claude has the enterprise. Perplexity has the citation depth. For brands the implication is simple: you don't pick which chatbot to optimize for, you track all of them — because the same brand-related query can produce a 615× difference in answer between platforms, and the same product's market share can read 76% or 38% depending on the panel. Multi-platform is the only honest way to read this market.

Grow your organic traffic from chat-bots

Track your AI visibility across ChatGPT, Gemini, Claude, and Perplexity — and turn chat-bot mentions into traffic.

Free to start

No credit card required

Setup in 60 seconds

Keep reading

Related posts

More articles on the same topics, prioritized by shared tags and keyword overlap.